In news– The RBI has recently released the results of its seven surveys. Each of these surveys throws light on some aspect or the other of the Indian economy.

Key findings of seven surveys-

- Consumer Confidence Survey (CCS)-

- The CCS asks people across 19 cities about their current perceptions (vis-à-vis a year ago) and one-year ahead expectations on the general economic situation, employment scenario, overall price situation and own income and spending. The latest round of the survey was conducted in July 2022.

- Based on the responses, the RBI came up with two indices: the Current Situation Index (CSI) and the Future Expectations Index (FEI).

- To read either index it is important to first understand that the value of 100 is the neutral level. An index below the 100 mark implies people are pessimistic and a value higher than 100 conveys optimism.

- As the CCS chart shows, the CSI (red dotted line) has been recovering since falling to a historic low in July last year.

- However, despite the improvement, the CSI stays firmly in the negative territory — suggesting consumer confidence is still considerably adrift from the neutral territory.

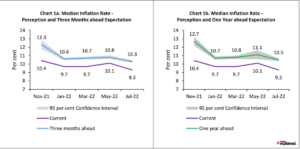

- Inflation Expectations Survey (IES)-

- It tracks people’s expectations of inflation. The biggest worry during phases of rapid inflation is that if inflation is not controlled soon, it can lead to people getting into the habit of expecting high inflation; that, in turn, alters people’s economic behaviour.

- This survey provides an answer to whether that is happening in India or not.

- OBICUS Survey-

- OBICUS stands for “Order Books, Inventories and Capacity Utilisation Survey”.

- This survey covered 765 manufacturing companies in an attempt to provide a snapshot of demand conditions in India’s manufacturing sector from January to March 2022.

- The key variable here is Capacity Utilisation (CU).

- A low level of CU implies that manufacturing firms can meet the existing demand without needing to boost production.

- That, in turn, has negative implications for job creation and the chances for private sector investments in the economy.

- The CU is well above the pre-pandemic level — suggesting India’s aggregate demand is recovering steadily.

- Industrial Outlook Survey (IOS)-

- Just like the CCS tries to suss out consumer confidence, this survey tries to track the sentiments of the businessmen and businesswomen.

- The survey encapsulates qualitative assessment of the business climate by Indian manufacturing companies for Q1:April, May and June and their expectations for Q2: July, August and September(2022-23).

- As per the IOS survey, businesses were optimistic (above the 100 level) in Q1, although not as much as they were in the recent past.

- But, they do expect things to improve as the months roll by. This tallies with the steadily improving capacity utilisation from the OBICUS.

- Services and Infrastructure Outlook Survey (SIOS)-

- Again, much like the CCS and IOS above, this survey does a qualitative assessment of how Indian companies in the services and infrastructure sectors view the current situation and the future prospects.

- This round of SIOS surveyed 758 companies on their assessment for Q1:2022-23 and expectations for Q2:2022-23.

- As per the SIOS, the companies in the services space are far more optimistic than the companies in the infrastructure sector.

- Bank Lending Survey (BLS)-

- This survey captured the mood — qualitative assessment and expectations of major scheduled commercial banks (SCBs) on credit parameters (viz., loan demand and terms & conditions of loans) for major economic sectors.

- The BLS found that the bankers’ assessment of loan demand in Q1 remained positive for all major sectors though the sentiments were somewhat toned down from the level reported in the previous quarter.

- Sentiments on overall loan demand in the second, third and fourth quarters also remained upbeat.

- Survey of Professional Forecasters (SPF)-

- It is the survey of 42 professional forecasters (outside the RBI) on key macroeconomic indicators such as GDP growth rate and inflation rate in the current year and the next financial year.

- India’s real GDP is expected to grow by 7.1 per cent in 2022-23 — projections revised down by 10 basis points from the last survey round— and it is expected to grow by 6.3 per cent in 2023-24.

- As per the survey the highest probability is that GDP growth will range between 7%-7.4%, the second most probable outcome is that the growth rate will decelerate to 6.5%-6.9% range.

Source: The Indian Express