In news– The centennial year of the Public Accounts Committee (PAC) was observed recently.

About Public Accounts Committee (PAC)-

- PAC is a committee of selected members of parliament, constituted by the Parliament of India, for the purpose of auditing the revenue and the expenditure of the Government of India.

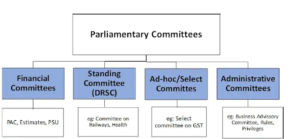

- It is one of the three Financial Parliamentary committees, the other two are the Estimates Committee and the Committee on Public Undertakings.

- It is the oldest Parliamentary Committee and was first constituted in 1921 in the wake of Montagu-Chelmsford Reforms.

- It consists of 22 Members, 15 Members are elected by Lok Sabha and 7 Members of the Rajya Sabha are associated with it.

- PAC is constituted every year under Rule 308 of the Rules of Procedure and Conduct of Business in Lok Sabha.

- The Speaker is empowered to appoint the Chairman of the Committee from amongst its Members.

- Till 1966-67, a senior member of the ruling party used to be appointed by the Speaker as Chairman of the Committee.

- In 1967, however, for the first time, a member from the Opposition in Lok Sabha, was appointed as the Chairman of the Committee by the Speaker. This practice continues till date.

- A Minister is not elected a member of the Committee.

Functions of PAC-

- Its function is to examine the accounts showing the appropriation of the sums granted by the House to meet the expenditure of the Government of India, the annual Finance Accounts of the Government of India and such other accounts laid before the House as the Committee may think fit except those relating to such Public Undertakings as are allotted to the Committee on Public Undertakings.

- Apart from the Reports of CAG on Appropriation Accounts of the Union Government, the Committee examines the various Audit Reports of the Comptroller and Auditor General on revenue receipts, expenditure by various Ministries/Departments of Government and accounts of autonomous bodies.

- The Committee looks upon savings arising from incorrect estimating or other defects in procedure no more leniently than it does upon excesses.

- In scrutinising the Appropriation Accounts of the Government of India and the Reports of the Comptroller and Auditor General thereon, it is the duty of the Committee to satisfy itself—

- that the monies shown in the accounts as having been disbursed were legally available for, and applicable to the service or purpose to which they have been applied or charged.

- that the expenditure conforms to the authority which governs it; and

- that every re-appropriation has been made in accordance with the provisions made in this behalf under rules framed by competent authority.

Source: PIB